McBride: What Buyers, Investors, and Cottage Seekers Should Know

Set in British Columbia's Robson Valley, McBride blends small-town practicality with deep mountain appeal. Whether you're considering a family home, a recreational cabin, or an acreage investment, the same core questions apply: zoning and permitted uses, infrastructure (well, septic, access), liquidity on resale, and seasonal factors that shape pricing and rental potential. Throughout this overview, I'll reference comparable markets and resources—including KeyHomes.ca—so you can calibrate expectations and run informed due diligence.

Market snapshot and lifestyle appeal

McBride sits along Highway 16 between Prince George and Jasper, with forestry, agriculture, and tourism shaping the local economy. Expect a quieter pace than larger Interior or coastal towns, with ready access to sledding, hiking, and river corridors. Amenities are modest, and trips to major centres for specialized services are part of the lifestyle.

Buyers commonly compare McBride with similarly positioned communities. For a regional contrast, reviewing Valemount market snapshots can help you benchmark pricing and inventory trends in the valley. On the waterfront cottage side, browsing Francois Lake waterfront listings offers a sense of how amenities and lake access influence values elsewhere in northern B.C.

Demand in McBride is highly lifestyle-driven. That can mean fewer multiple-offer situations than urban hubs but also longer average days on market, especially in winter. Investors should model conservative absorption timelines and carry costs.

Zoning, ALR, and rural regulations

McBride properties fall under the Village of McBride and the Regional District of Fraser-Fort George (RDFFG). Zoning varies by parcel (e.g., Rural Residential, Agricultural), and portions of the area lie within the Agricultural Land Reserve (ALR). Before removing conditions, verify zoning, ALR status, and site-specific setbacks with RDFFG and the Village office. In the ALR, non-farm uses, additional dwellings, and short-term rental (STR) activity face added scrutiny. Some small secondary dwellings are possible under provincial ALR rules, subject to size/location limits and local bylaws—confirm with the Agricultural Land Commission and RDFFG planners.

Riparian and floodplain considerations matter near creeks and the Fraser River; the Riparian Areas Protection Regulation can trigger environmental reports and setbacks. Ask your agent for available floodplain mapping and past permits. Wildfire risk is another practical lens: home insurers increasingly price based on FireSmart defensible space, roofing and siding materials, and road access/egress.

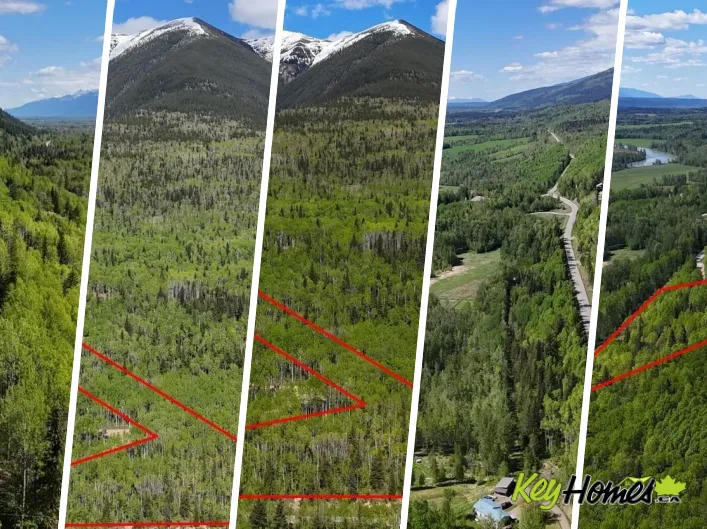

Access and road type—including “mcbride timber road”

Some rural parcels rely on resource or seasonal roads. Forestry or spur routes—often described informally (e.g., “McBride Timber Road,” commonly referenced as mcbride timber road)—may have variable maintenance or winter plowing. Confirm legal access on title (not just “we always used that road”), and speak with the road authority about year-round reliability. Access uncertainty can affect financing and resale.

Financing and insurance nuances

Rural financing is fundamentally about collateral quality and risk management:

- Wells: Lenders typically require potability testing and may ask for a recent flow test. A 4–5 gpm sustained flow is a common comfort threshold, but requirements vary by lender and usage.

- Septic: Expect a compliance letter or inspection by a registered practitioner; maintenance logs help.

- Acreage: Lenders value the residence first; outbuildings and large land bases contribute less to the loan-to-value ratio. High-acreage or hobby-farm configurations may need more down payment.

- Manufactured/log homes: Insurers and lenders can be selective. Manufactured homes usually need CSA labels and permanent foundations; log homes sometimes trigger insurer questions on maintenance and settlement history.

- Heat sources: Wood stoves often require a WETT inspection; older oil tanks can be an underwriting red flag.

- Radon: Interior B.C. has elevated radon potential. Testing is inexpensive; some lenders and buyers now view mitigation as routine due diligence.

If you're comparing ownership forms, note that cooperative titles are financed differently than fee simple or strata. Reviewing Vancouver co‑op ownership examples can clarify why mainstream lenders cap exposure or require higher down payments—useful context even if your McBride target is fee simple.

Seasonal market trends and comps

Activity in McBride generally peaks from late spring through early fall. Trails are open, acreages show better, and out-of-region buyers travel more easily. Winter can be quieter, but serious buyers who need year-round access may be more motivated. For apples-to-apples pricing, study small-town comparables rather than big-city averages. It can still be instructive to examine urban baselines—say, the pricing dynamics on Dallas Road, Victoria waterfront homes or the renovation premiums around Edmonton historic homes—to understand how location liquidity and buyer pools make a difference.

For rural benchmarks, browsing acres in the Cariboo or Stone Mills rural properties offers context on how distance to services, topography, timber value, and utility availability translate into price per acre. These are not direct comps, but they do sharpen your valuation instincts across similar property types.

Investment and short‑term rental rules

British Columbia's Short‑Term Rental Accommodations Act (phased in 2023–2025) introduces a principal‑residence requirement in designated communities and gives municipalities sharper enforcement tools. McBride is a small community and may not be designated; however, local business licensing, occupancy limits, and quiet‑hour rules can still apply. If your business model includes nightly rentals, confirm with the Village of McBride and RDFFG before you write an offer. Platform compliance and a provincial registry are ramping up—be prepared to show ownership, zoning compliance, and tax registration.

For lake‑centric STRs, note how access and seasonality shape rates and occupancy. Compare the dynamics you'd expect at destinations like Weslemkoon cottages or the broader northern‑lakes circuit showcased by Francois Lake waterfront listings. Amenities, road plowing, and winterized infrastructure influence year‑round viability.

Tax and policy lens: McBride is outside B.C.'s major speculation/vacancy tax areas. The federal foreign buyer ban (extended to 2027) targets CMAs/CAs; rural communities like McBride are generally outside those zones, but confirm boundaries with your lawyer because definitions are technical and occasionally updated.

Resale potential, liquidity, and exit planning

Small markets trade on unique value rather than broad buyer pools. That means two things:

- Liquidity risk is real: Expect longer hold periods and plan contingencies. Staging a home with good winter access and clear maintenance history can help shorten days on market.

- Market shocks can be amplified: Employer changes, mill closures, or highway projects can swing local demand more sharply than in diversified cities.

When benchmarking exit potential, compare different buyer catchments. The GTA's Highway 50 Castlemore corridor or the Meadowvale–Scarborough area demonstrate how large urban markets can absorb listings quickly, while small‑town B.C. needs pricing precision and patience. Within the Robson Valley, monitoring homes in Valemount provides additional real‑time signals for buyers eyeing McBride as an alternative.

Practical due diligence for McBride buyers

- Title and access: Confirm legal road access and any registered easements. Don't rely on historic use alone.

- Water and septic: Obtain recent well potability/flow tests and septic documentation. Budget for upgrades if results are marginal.

- Environmental: Check RAPR setbacks, floodplain maps, and wildfire risk mitigation. Walk the property boundaries; verify with a survey if in doubt.

- Structures and permits: Ensure additions, decks, wood stoves, and outbuildings have permits where required.

- Zoning and ALR: Match your intended use (home‑based business, additional dwelling, STR) to permitted uses. Get written confirmation from the local authority.

- Insurance and financing: Pre‑consult with your insurer and lender if the property includes log construction, older fuel systems, or limited winter access.

- Community fit: Visit at different times of day and season; assess road maintenance, cell coverage, and noise (rail/highway).

When researching online, you may encounter threads or names—such as “rhys edworthy”—circulating in market discussions. Treat all third‑party commentary as a starting point and verify locally with licensed professionals.

How KeyHomes.ca fits into your research

For a small market like McBride, credible data points are everything. KeyHomes.ca is a practical place to compare rural listings across regions and to connect with licensed professionals who understand zoning, wells/septic, and ALR nuances. As you calibrate expectations, it helps to triangulate McBride with other geographies—whether you're studying larger acreages in the Cariboo or testing urban liquidity proxies via heritage streets in Edmonton. The same platform also offers coastal/urban contrasts—like Dallas Road, Victoria—so you can see how buyer pools and amenity sets change pricing and absorption.

Scenario examples specific to McBride

Owner‑occupied acreage: You find a 10‑acre parcel with a 1990s log home and a detached shop. Your lender requests a full appraisal, well potability test, and a WETT inspection for the wood stove. The appraiser attributes limited contributory value to the shop and land beyond the home site. You adjust your down payment plan accordingly and negotiate a credit for a marginal well flow result.

Seasonal cabin: A recreational cabin up a resource road looks perfect, but winter plowing is sporadic. The access is via a statutory right of way across a forestry lease, not fee‑simple road frontage. You confirm with the road authority and your insurer that winter response times are uncertain, and you price that risk into your offer. You also verify whether the Cabin's EC zoning permits nightly rentals, given evolving provincial STR rules.

Urban trade‑off: You're weighing a McBride move against a city purchase. Looking at the liquidity and amenity trade‑offs in places like Meadowvale–Scarborough helps you understand exit timing differences. Likewise, rural contrasts such as Stone Mills reinforce how utility availability and distance to services influence valuation. If an alpine vibe is non‑negotiable, browsing Valemount may confirm your preference.

Key takeaways for McBride buyers and investors

Verify first, speculate later. The most successful purchases in McBride start with precise checks on zoning/ALR status, access rights, and water/septic performance. Plan for seasonal realities—road maintenance, heating, and rental regulation timelines—so you're not surprised post‑closing. And if you're eyeing a property near industrial or forestry activity (including corridors referenced as “mcbride timber road”), consider long‑term access and noise in your budget and your exit strategy.

Balanced research across regions—using resources like KeyHomes.ca and selectively reviewing markets from northern lakes to urban cores—will keep your expectations grounded and your financing, insurance, and resale planning on track.