Mortgage helper Richmond: what buyers and investors should know

In Richmond, British Columbia, a “mortgage helper” typically refers to a self-contained secondary suite or accessory dwelling that generates rental income to offset carrying costs. With rising rates and limited rental supply across Metro Vancouver, demand for legal income suites has grown. This article outlines how to evaluate a mortgage helper Richmond opportunity—zoning and permits, financing, resale, lifestyle appeal, and seasonal/ regional considerations—using practical examples. Where regulations vary by municipality or change over time, confirm locally with the City of Richmond and your legal and mortgage advisors. For market comparables and planning research, many buyers start at KeyHomes.ca to explore listings and data.

Zoning, permits, and compliance in Richmond

Most single-detached areas in Metro Vancouver municipalities permit one secondary suite, subject to zoning and the BC Building Code. In Richmond, suites typically require a building permit (for new work or to legalize existing), a separate exterior entrance, egress windows, smoke/CO alarm interconnection, and fire-rated separations. Expect inspections for life-safety, electrical, heating, ventilation, and plumbing. Secondary suites are generally limited by the BC Building Code to a maximum of 90 m² (about 968 sq. ft.) and no more than 40% of the principal dwelling's floor area, but always verify the current code and local bylaws. Some municipalities require on-site parking for the suite and may set lot size or frontage minimums.

Coach houses, garden suites, and other detached accessory dwellings may be more limited and can require rezoning or a site-specific permit. If a listing advertises a “suite” without permits, the unit may be an unauthorized accommodation; lenders and insurers will treat it differently. When in doubt, obtain a municipal compliance letter and compare against plans and permits.

Short-term rentals (STRs) and suite use

BC's Short-Term Rental Accommodations Act restricts STRs in designated communities to a host's principal residence (with limited allowances for one secondary suite or accessory dwelling, subject to local bylaws and licensing). Richmond bylaws are stricter in some cases, and strata corporations can prohibit or further restrict STRs. Do not underwrite a Richmond mortgage helper on nightly rental income without written confirmation of local and strata rules. Long-term rentals remain governed by the Residential Tenancy Act (RTA), including annual rent increase limits set by the province.

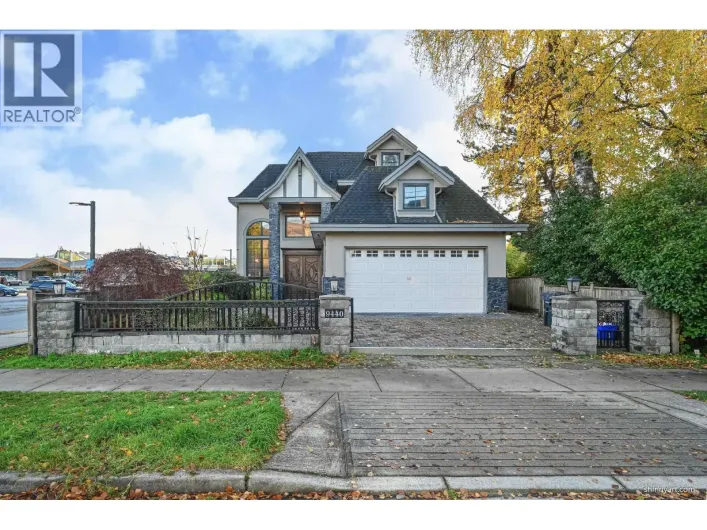

Suite types and property formats

Secondary suite in a single-detached house: The most common mortgage helper configuration. Best candidates offer grade-level light, proper ceiling heights, independent laundry, and acoustical separation. Proximity to the Canada Line or major employers improves demand.

Duplex or stratified multi-unit: Offers higher rent potential and clearer unit separation, but may cost more up front. For multi-market comparisons, studying a well-located low-rise apartment in Downtown Vancouver can help benchmark cap rates versus ground-oriented Richmond rentals.

Accessory dwelling (coach house/garden suite): Viability depends on lot size, servicing, and zoning. These can command a “privacy premium” from tenants, but permitting is more involved.

Financing a home with a legal suite

Most A-lenders and insured lenders will include a portion of market rent when calculating your debt service, but the method varies:

- Rental offset: a percentage of gross rent (often 50–70%) reduces housing costs used in GDS/TDS ratios.

- Rental add-back: a percentage of rent is added to your income. Some lenders will use 100% add-back if the suite is legal and self-contained.

Example: If the suite can achieve $2,100/month and your lender allows a 50% offset, $1,050/month lowers your effective mortgage payment for qualification. If using an add-back, $2,100 could be added to income (subject to lender policy). Lenders typically require a lease or market rent appraisal and may insist the suite is legal with permits. Unauthorized suites often see more conservative income treatment.

If you are comparing adjacent markets for price relief or yield, reviewing a curated page of mortgage-helper homes in Burnaby can highlight how lender treatments and rents affect purchasing power across municipal lines.

Resale dynamics and valuation

Legal suites add value by expanding the buyer pool—first-time buyers needing payment support, multi-generational families, and investors seeking resilient rent. Appraisers give the most credit to suites with:

- Documented permits and final inspections (no outstanding work orders).

- Code-compliant life-safety (egress, smoke/CO interconnects) and separated systems.

- Independent access, sound attenuation, and functional layouts.

Unpermitted or “in-law” accommodations may still trade, but discounts for risk and remediation are common. If flood construction level (FCL) rules were triggered during renovations, ensure documentation—Richmond's floodplain context means building heights, foundation design, and mechanical placement can affect both insurance and future redevelopment potential.

Lifestyle appeal and tenant demand in Richmond

Richmond's draw includes the Canada Line, strong retail corridors, YVR adjacency, and diverse dining. For suites, transit access and on-site parking are key. Assess aircraft noise corridors near Sea Island and consider soil conditions; parts of Richmond have soft soils, which can influence seismic upgrades and buyer comfort. The city's diking and drainage program is robust, but insurers will underwrite flood exposure differently—obtain quotes early and budget for deductibles specialized to the area.

For families, proximity to schools and parks increases demand. For multi-generational living or mobility needs, properties with accessibility features—like a home incorporating an elevator—can future-proof occupancy and broaden the resale audience.

Seasonal and regional considerations for cottage and hybrid buyers

Many Richmond buyers also consider “hybrid life” options—keeping a primary home with a suite and adding a recreational property on Vancouver Island or the Sunshine Coast. If your mortgage helper covers part of the mortgage, the incremental carrying cost for a modest getaway can become workable.

On Vancouver Island, strata-townhome clusters such as Wembley in Parksville offer lower-maintenance living convenient for seasonal use. Loft-style spaces—see a Vancouver Island loft example—can attract long-term tenants during shoulder seasons. Waterfront markets, like Comox waterfront homes, can command premium weekly rents, but confirm local STR bylaws and the provincial principal-residence rules. For truly remote experiences, properties on Nootka Island demand careful planning for access, insurance, and maintenance.

Rural or semi-rural properties may rely on wells and septic. Budget for potability testing, flow rate verification, and a septic inspection with recent pump-out records. In off-grid or raw land scenarios—such as acreage with water features—lender options narrow; private financing or larger down payments are common. Storage and vehicle flexibility matter if you split time between properties; a home with dedicated RV parking in Langley can alleviate seasonal gear clutter.

Tenancy, taxes, and bylaws to watch

For long-term rentals, the RTA governs security deposits, notices, and rent increases. The annual rent increase limit is set by the province; check the current year's cap. Fixed-term tenancies typically roll to month-to-month unless otherwise permitted by law. Strata bylaws can restrict rentals and occupancy; review them for suite permissions, minimum term length, and noise/parking rules.

Taxes: Richmond falls under BC's Speculation and Vacancy Tax (SVT). Familiarize yourself with SVT declarations, exemptions, and how they differ from Vancouver's municipal Empty Homes Tax (which does not apply in Richmond). If you plan periodic personal use of a second home, ensure you remain compliant with SVT to avoid unexpected charges.

Design and operating tips for durable suites

- Sound and privacy: resilient channel, insulation, solid-core doors, and well-located mechanicals reduce noise complaints.

- Independent systems: separate heating controls, dedicated laundry, and clearly metered utilities (even if sub-metered) simplify management.

- Light and safety: maximize natural light, add exterior lighting and wayfinding; ensure proper egress and handrails.

- Documentation: keep permits, final inspections, and contractor warranties organized for refinancing or resale.

If you track urban investment comps outside BC as part of your research, studying an Empress Walk condo in North York can contextualize how rent control and carrying costs differ across provinces—useful for portfolio-level decisions.

Market timing and seasonal patterns

Richmond's detached market with suites is active year-round, with listing peaks in spring and early fall. Investor demand often intensifies ahead of mortgage renewals as owners seek to rebalance cash flow. Seasonal cottage markets, by contrast, see activity ramp from late winter through midsummer, when access and weather improve. If you're buying a principal residence with a suite and planning a recreational purchase later, consider locking suite rents before the summer cottage rush to stabilize debt ratios during your second acquisition.

Due diligence checklist for mortgage-helper homes

- Verify zoning and permitted suite type; obtain municipal compliance letters and copies of permits.

- Confirm building code items: ceiling height, egress, smoke/CO interconnects, fire separations, ventilation.

- Underwrite conservative rents using a market rent appraisal; stress-test with a vacancy allowance.

- Get insurance quotes for landlord coverage; add host coverage if any permitted STR use will occur.

- Review strata bylaws (if applicable) for rental/STR rules and parking allocations.

- Request a recent Property Disclosure Statement (PDS) with suite details and any electrical or gas permits.

- Consider floodplain, FCL, and soil conditions; budget for seismic/foundation considerations in older homes.

As you compare “homes for mortgage” support across Metro Vancouver and beyond, leverage data and verified listing details. Resources like KeyHomes.ca—whether you're studying an inner-city low-rise benchmark or specific neighbourhood inventory—help normalize assumptions. For example, contrasting Richmond suite cap rates with a downtown Vancouver low-rise investment can clarify where your risk-adjusted yield sits relative to transit, amenities, and tenant profiles.